Terrible time lag

Source: WeChat public number lixunlei0722

The inventory cycle is difficult to change the economic downturn

Today, a reporter called to ask: Why is steel prices falling when all kinds of economic data are so good? I replied that I lacked an in-depth study of steel prices, which may be caused by inventory factors – when steel or iron ore stocks are low, as long as the demand at the bottom increases, the need to replenish stocks increases simultaneously, which leads to The actual demand has grown exponentially, and vice versa. Steel prices have risen from the lows at the end of 2015 and have risen for more than a year. Presumably, they have accumulated a lot of stocks and there is pressure to destock.

Since economic activities have a conduction process between the upstream and downstream, and between the inside and the outside, a "time lag" phenomenon occurs. In addition, because the conduction speed is fast and slow, the "time lag" is also long and short. For example, in nature we always see lightning first, then hear thunder, because the speed of light is much faster than the speed of sound, so there is a time lag between lightning and lightning. However, many people are afraid that the roar of thunder is more than the lightning that has passed through the sky, but in fact thunder does not have lethality, and lightning is a truly destructive force.

It is precisely because of this "time lag" of economic activities that people are often confused by appearances and even lead to decision-making mistakes. For example, for this round of cyclical industry recovery, many people think that the rise of the new round of economic cycle, then why is it not a short-term rebound in the mid-long period of economic downturn? The high point of China's economic growth appeared in 2007. After the US subprime mortgage crisis in 2008, China launched a two-year, four trillion yuan infrastructure investment stimulus policy, which basically ended in 2011, but with the economic growth. As the speed went further, the government finally launched a new round of economic stimulus in mid-2012.

A typical case is the afternoon of May 27, 2012. The National Development and Reform Commission officially approved the construction of the Zhanjiang Iron and Steel Base project in Guangdong. The mayor of Zhanjiang was unable to suppress the kiss and approve the documents in front of the National Development and Reform Commission.

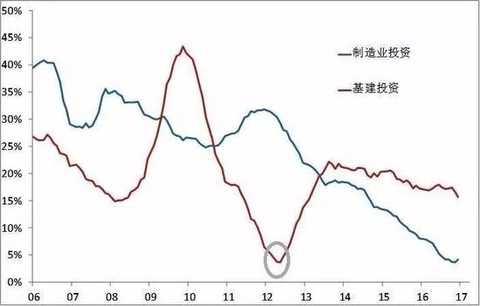

Source: WIND, courted by Wang Xiaodong, Zhongtai Securities Research Institute

Source: WIND, courted by Wang Xiaodong, Zhongtai Securities Research Institute

Since 2013, China's infrastructure investment (excluding electricity, heat, gas and water production and supply) has rebounded again, with an investment scale of 7.1 trillion yuan, and 8.7 and 10.1 in the following three years (2014-16). And 11.9 trillion yuan, maintaining a high growth rate of more than or nearly 20% for four consecutive years, but the growth rate of manufacturing investment fell sharply in the same period, from 22% in 2012 to 4.2% in 2016. At the same time, GDP growth rate also dropped from 7.7% in 2012 to 6.7% in 2016, indicating that although the government is trying to achieve steady growth through large-scale infrastructure investment, the actual effect is not satisfactory.

However, the mid-upstream industry has been going to capacity and stimulating demand for several consecutive years, which will inevitably lead to an increase in the prices of production materials in the middle and upper reaches. For example, at the end of 2015, the prices of a number of bulk commodities such as steel began to move, but the macro-level stimulus policies did not. Do not dare to slack off, the credit scale in the first quarter of 2016 reached 4.6 trillion yuan, exceeding the scale of 2009 in response to the subprime mortgage crisis. Therefore, despite the good signs of the economy, the existence of time lag has led to excessive policy stimulus. Not only is the decision-making layer difficult to grasp the economic hot and cold, but private enterprises are also difficult to make correct judgments. For example, in the first quarter of 2016, private investment has experienced a cliff-like decline, which is equivalent to “selling at the short-term low point of economic growthâ€. ".

It is not difficult to find that the PPI's year-on-year data has been negative since March 2012 and lasted for more than four years. It was not until the September of 2016, but the PPI's ring data began to turn positive in March 2016. In general, the overall behavior of private investors in the real economy is not much different from the overall behavior of retail investors in the capital market, that is, they are chasing up and down. One of the important reasons is the time lag factor, if it continues to be huge Investing does not achieve the desired results after a period of time, which makes people more pessimistic about the economy.

Today, whether it is official or private, everyone seems to have confidence in the future economy, because the published data is very beautiful. For example, in January-February this year, the total profits of industrial enterprises above designated size increased by 31.5% year-on-year, even the export was 3 The month has increased by 16.4%, setting a new high in two years. In addition, indicators such as power generation and rail freight volume have also reached new highs for many years, but most of this data can be attributed to the lagging response from sustained economic stimulus since mid-2012.

Behind the gorgeous data, we need to pay attention to two aspects: one is the time lag factor, and the other is the input factor. The time lag factor is no longer described, and the research input factor is to examine the input-output ratio. The improvement of various economic indicators since the second half of 2016 is related to the government's debt collection, high investment by state-owned enterprises and residents' leverage. With the substantial expansion of credit of commercial banks, such as the short period of four years in 2012-2016, the total number of commercial banks Assets have increased by 100 trillion yuan, which includes huge amounts of information such as credit expansion of state-owned enterprises, debt replacement by local governments, and PPP.

Of course, from another point of view, it also shows that the Chinese government has a very strong ability to organize resources. This is far beyond the reach of Western governments. For example, in 2016, the investment of the Chinese government and state-owned enterprises accounted for nearly 40% of GDP. US government investment accounts for about 10 times of GDP. From this perspective, we do not seem to worry too much about the ability of the government to grow steadily in the next few years, but it is difficult to change the downward trend of the economy. Moreover, in the short term, the inventory cycle seems to have entered the destocking phase.

Excavator sales are definitely not a leading indicator

In March 2017, excavator sales increased by 56.2% year-on-year, and excavator sales in the first quarter increased by 98.87%. In absolute terms, excavator sales in the first quarter of this year are close to the same period in 2012. According to the construction sequence of the project, the excavator sales growth will be gradually transmitted to other construction machinery and equipment. In the first two months of the year, the crane sales growth rate exceeded 130%, and the loader sales growth rate exceeded 60%.

Further enquiry data found that 2011 was the highest peak of China's excavator sales, reaching 183,500 units in the year, 35% in 2012, 3% in 2013, 19% in 2014, and 37% in 2015. The annual growth rate is 25%. That is to say, when China's economic growth rate fell in 2011, the sales volume of excavators hit a historical peak with a lag of one year. In 2013-2015, the high growth of infrastructure investment for three consecutive years failed to change the decline in sales volume. It was not until 2016 that the economic recovery and sales rebounded.

What is the main reason for the sharp increase in sales of excavators?

Source: WIND, Photo courtesy of Shengtai Securities Research Institute

Source: WIND, Photo courtesy of Shengtai Securities Research Institute

Although the mini excavator has the highest proportion, this ratio has not changed significantly since this cycle. The biggest improvement is the large excavator of more than 30 tons, and the large excavation is mainly used in the mining industry. Therefore, the increase in infrastructure and real estate investment relative to upstream demand is not high, and the demand expansion of the upstream extractive industry is the most significant.

I have not studied the construction machinery industry including excavators, but I have encountered three interesting things. The first thing is that in 2011, one of my graduate students who made equity investments called me and said that he is working with a lot of PEs to compete for shares in a hydraulic equipment company. This company has unique patented technology. And the order was too late to do. What's more, the chairman of the company happened to be my high school classmate - he encouraged me to invest in the company with him. It is a pity that I am a risk-averse person, although I know that there is no interest in it. Last year, I met this graduate student and asked if the company he invested in was listed. He was very helpless. Because the company’s performance was not satisfactory, it could not be listed. This shows that investing in cyclical industry timing is very important, and the risk of choosing a profitable high point for investment is high.

The second thing also impressed me: my high school math class representative, in 2012, actually gave up the enviable position of the chief engineer of the Ford Motor Company in the United States, went to a famous domestic construction machinery company to develop large engine. But in the end, he left the Chinese company and taught at the university. I didn't ask him why he left. He wondered if this Chinese company introduced a large number of talents at a high profit point, but at the dawn of the dawn, it cut R&D expenses and cut high-end talents.

The third thing gave me a deeper impression: In November 2014, I was fortunate enough to be invited to participate in the symposium of Prime Minister Ke Qiang, and the chairman of Zoomlion, who attended the symposium. Prime Minister Keqiang discussed with him many ways to solve the problem of overcapacity in the construction machinery industry, such as exporting to Africa, and hope that China's traditional industries can “make new treesâ€. However, from the data point of view, the construction machinery industry in 2015 is even more difficult than in 2014. Although the capital investment has maintained high growth for the third consecutive year, once the trend is formed, there is basically no way to do it.

The above three stories show that due to the existence of time lag factors, what we see is not necessarily a prelude to the fascination, it is probably the most gorgeous curtain call. Like a deafening thunder, although it may scare people away, it has no lethality. The past 2016 is likely to be the year with the strongest economic stimulus policy in China. Although there is a Belt and Road Conference this year, there is a boom in the construction of Xiong'an New District, but the growth rate of infrastructure investment may not exceed last year.

It has been mentioned that the increase in sales of excavators is related to the equipment renewal cycle, which is not unreasonable. There is a saying that the equipment update period is equal to the sum of two inventory cycles, ie 6-8 years. This reminds me of the reason for the surge in car sales last year, and it is also related to the renewal cycle of automobiles. With the growth of the scale of ownership, the demand for car replacement has become more and more supportive for sales. Generally speaking, 70-80% of used cars have a service life of less than 6 years, and the average replacement period of vehicles is about 3 years, and is currently at the end of a replacement cycle. Superimposed car scrap subsidy policy and purchase tax preferential policy for demand overdraft, 2017 car sales may not be optimistic. In the first quarter of this year, car sales increased by only 7%, and the negative growth in passenger car sales also partially confirmed this.

Similarly, the momentum of high sales growth of excavators and other construction machinery is estimated to last for a long time. First of all, this year's excavator sales are hot again, and it is estimated that it is difficult to exceed the sales in 2011, although the nominal size of infrastructure investment this year is estimated to be twice that of 2011. Secondly, this round of inventory cycle rebound is very limited, because this is a weak rebound in the context of overcapacity in the whole society. As the downstream reaches, the demand is weaker.

High housing prices are also a time lag

At the moment, those who believe that house prices will not fall should account for the majority. From the perspective of statistical laws, the consensus expectations of most people are always wrong when judging market trends.

I remember that at the beginning of 2003, someone told me that the house prices in the United States have risen for ten years and should not fall. I have observed it for a few years, and sure enough. In 2005, even the conservative Fed Chairman Greenspan testified to Congress that it was rare to say that "the United States has not yet had a national real estate bubble." Although everyone was more consistent about the existence of bubbles at the time, some economists described it as “beer foam and coffee (Cappuccino) foamâ€, which would not “secate†each other and form a bigger bubble. Various places also regulate the market according to local conditions, forcing the bubble to slowly recede. Some economists believe that “diversification of loan channelsâ€, “diversification of product mixâ€, “diversification of loan interest rates and multiple choices of refinancing mechanisms†and “diversified trends in real estate consumption structure†make the bubble not Broken.

Unfortunately, it is in this consensus that 2006 US housing prices have seen a downward trend. In August 2007, the subprime mortgage crisis swept the financial markets of the United States, the European Union and Japan. People are always used to finding reasons for the status quo. We are now also the same. If there is a bubble in the real estate market with Chinese characteristics, the house price will never fall because the land is regulated, that is, the supply is limited and the state has the ability to regulate. This is not the same as the American people’s understanding of the “American-style†real estate market that will not fall in 2005.

In fact, in this round of US real estate bull market since 1993, the high point of real estate development investment growth occurred in 2000, but the house price decline occurred in 2006, indicating that the inflection point of house price lag behind investment growth began to fall in six years. The high point of China's real estate development investment growth rate in 2010, reaching 33%, has now fallen back to single digits, indicating that real estate as a cyclical industry will certainly undergo a process from prosperity to recession, but it is difficult to predict the specifics of the recession. time.

The rebound with this short-term economic cycle was finally achieved through continuous stimulus policies. The PPI experienced a negative growth of four and a half years before it turned positive. Similarly, the policy of regulating real estate has been implemented very early, but the effect has been very unsatisfactory. Since the second half of last year, the state’s regulation of housing prices should be the most severe in so many years – “the house is used for housing, not for speculationâ€, and measures such as purchase restriction, limit loan, and price limit are becoming more and more More cities are launched. If housing prices continue to rise in 2017 and in the next few years, the real estate policy will continue to tighten. This will mean that the housing price bubble will be more and more blown. Once it breaks down, it will definitely have a greater lethal effect on the economy. Diving in the three-meter springboard, I will have to jump down on the 10-meter platform in the future.

The bursting of the housing price bubble is hard to avoid in almost any country, although policymakers do not want this to happen. However, due to people's limited cognitive ability, it is prone to overcorrection in policy regulation. For example, as early as 2003, the relevant ministries and commissions jointly issued a document ("Notice on Stopping Some Opinions on Blind Investment in the Iron and Steel Electrolytic Aluminum Cement Industry" - No. 102), "At present, the three industries of steel, electrolytic aluminum and cement are under construction. The production capacity of the project greatly exceeds the expected demand, which will inevitably lead to overcapacity, disorderly market competition, waste of resources and environmental pollution, and even financial risks and other hidden dangers in the economic and social sectors.

In fact, China's steel production capacity in 2003 was less than 300 million tons. From 2003 to 2007, China was in the period of rapid development of heavy industrialization, and the production limit was not timely. Today, only Hebei's steel production capacity exceeds 300 million tons, and the country exceeds 1.2 billion tons. It can be seen that the judgment of expected demand is often difficult to be accurate, and the actual demand greatly exceeds expectations. In addition, Hebei, the water-deficient province that should limit the development of steel enterprises, has the largest scale of capacity expansion, which has also brought about Beijing-Tianjin-Hebei. Serious pollution in the area.

However, the passivation of the regulatory policy does not mean that the time lag effect of the policy will not occur. The most terrible thing is that so many regulatory policies continue to accumulate, and eventually the phenomenon of “the last straw crushing the camel†may occur. Since the rise in housing prices is essentially a demographic phenomenon, according to the Ministry of Human Resources and Social Security monitoring data on rural labor transfer in 500 villages, the number of migrant workers in the first quarter of this year was 279,000, a year-on-year decrease of 2.1%. This should be the first negative growth of migrant workers in China since the reforms of the 1980s, and the decline in China's floating population occurred in 2015. In addition, the decline in the number of 25-45-year-olds who are the main buyers of home buyers also appeared in 2015. I also found that in the past, Anhui, as a province with a net outflow of population, increased its permanent population by more than 600,000 last year, which means that the population inflows of other developed provinces or large cities are slowing down or even decreasing. So where does the driving force behind the rise in housing prices come from? In addition to monetary expansion factors, other explanations such as improving demand are not strong.

The factors that have an inhibitory effect on housing prices, such as population aging and negative population growth, have not fully demonstrated their effects. I think it is also a time lag phenomenon. The rise or fall of the price of capital goods will form a trend. Once the trend is formed, its inertia will greatly exceed that of consumer goods. This is because investors' profitability and irrationality exceed consumers. This is the case when house prices are rising. Once it falls, I believe so. The view that house prices will only rise, not fall, or fall is only a small adjustment is widely accepted because the current housing prices are in the midst of rising inertia, thus neglecting the negative forces are constantly strengthening.

In the real estate bull market in the United States from 1993 to 2006, the average annual increase in house prices was about 6%. In the 2006-2008 subprime mortgage crisis, the cumulative decline in national house prices averaged around 20%, and individual cities were even close to 50%.

In the decade from 2000 to 2010, China's house prices rose the fastest, with an average annual increase of more than 15%. After 2011, house prices have transitioned from general to structural growth, with a cumulative increase of 40% in six years (100 cities announced by the China Index Research Institute). House price-weighted index), although the late growth rate slowed down, but the cumulative increase far exceeds the last round of real estate bull market in the United States. For example, the cumulative increase in house prices in the north and the west is estimated to be more than 15 times. In addition, the growth rate of residential mortgage loans has been accelerating over the years. In 2016, new residential mortgage loans reached 4.96 trillion yuan, and urban residents spent 23% of the total disposable income of urban residents in the year. More than 60% of the loans of the four major banks are residential mortgages. Residents buying houses and levers are so fast, is it a bit of a taste of subprime inflation in the United States?

When the residents department purchases a large proportion of debts, their consumption power and demand will be weakened. Therefore, the CPI has been below 1% for two consecutive months. This is called the so-called hoist. Therefore, do not underestimate the effect of time lag. The social economy is a big system, and investment and consumption tend to be different. When you notice that there are several asset price bubbles, the bubble has already spread, and the control is only a small part of the big system.

Enter [Sina Finance and Economics Unit] Discussion

Kids Slipper Socks,Childrens Christmas Slipper Socks,Christmas Slipper Socks,Childrens Slipper Socks

JINGJIANG SHIJIA INTERNATIONAL TRADING CO.,LTD , https://www.jjsjinternational.com